I am surprised at how little coverage Argentina’s sovereign default has earned. The Financial Times even notes something of a post-default calm in financial markets (although it also warns of choppy seas ahead). One reason may be that the default has been anticipated for so long—given Argentina’s history of sovereign default—that it’s not really news. Another might be that sovereign defaults are a bit abstract for everyone but creditors and the citizens of the defaulting countries.

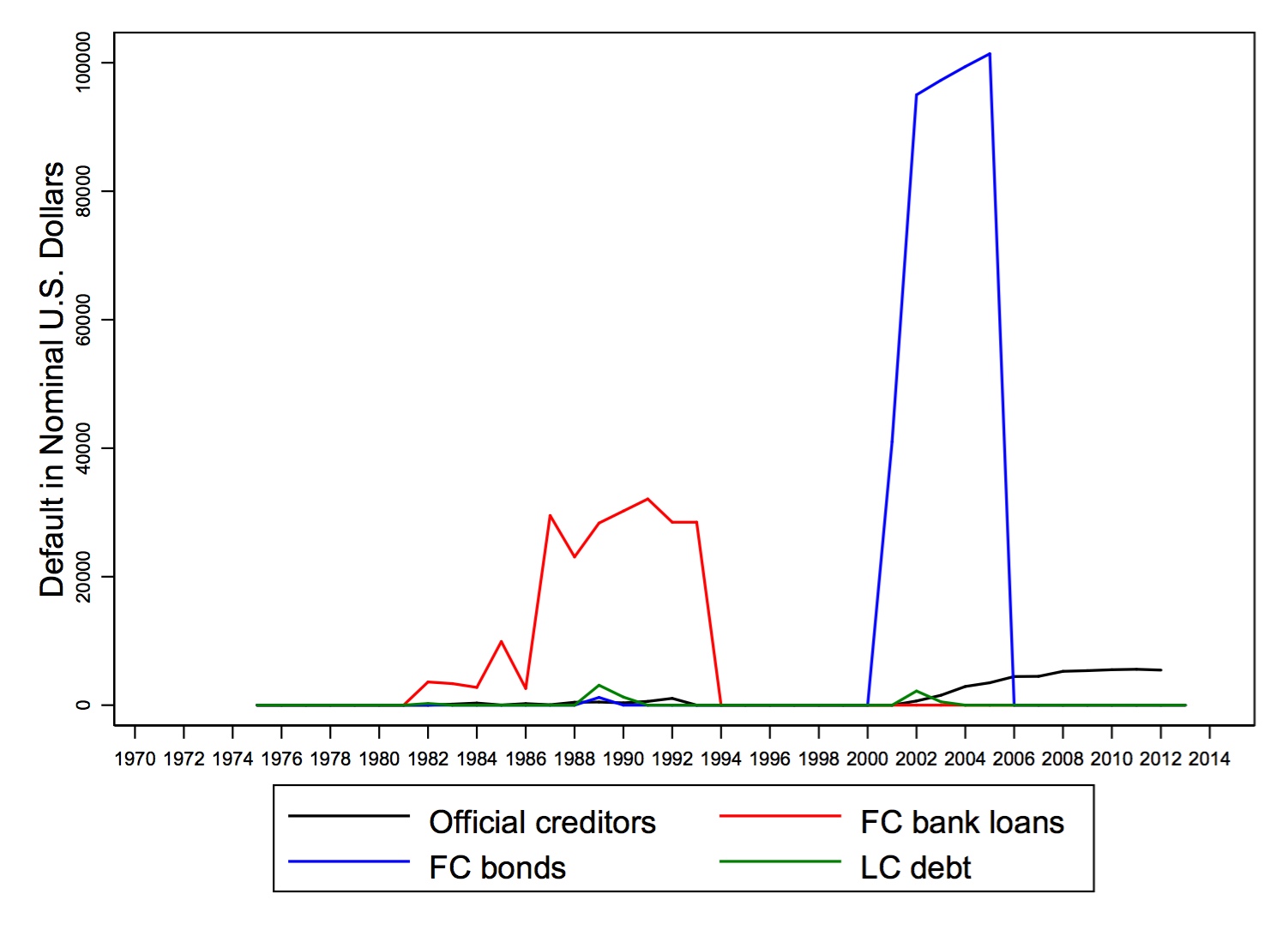

One useful new source for some data that can put Argentina’s default into perspective is a dataset from the Bank of Canada described in this report by Beers and Nadeau. Unlike the more comprehensive financial crisis data from Reinhart and Rogoff, which extends much further back in time in addition to covering more types of crises, the Beers and Nadeau data cover many more lower- and middle-income countries. They also usefully distinguish among various types of sovereign default according to who actually holds the debt. If we plot the data for Argentina, here is what we find:

The 1980s and early 2000s debt crises are readily apparent here, as are the differences between the two. The data also help to remind us that unlike personal bankruptcy, defaults endure. We also see original sin in action: Argentinian defaults do not involve LC (local currency) debt because Argentina/Argentinians cannot borrow abroad in their local currencies.

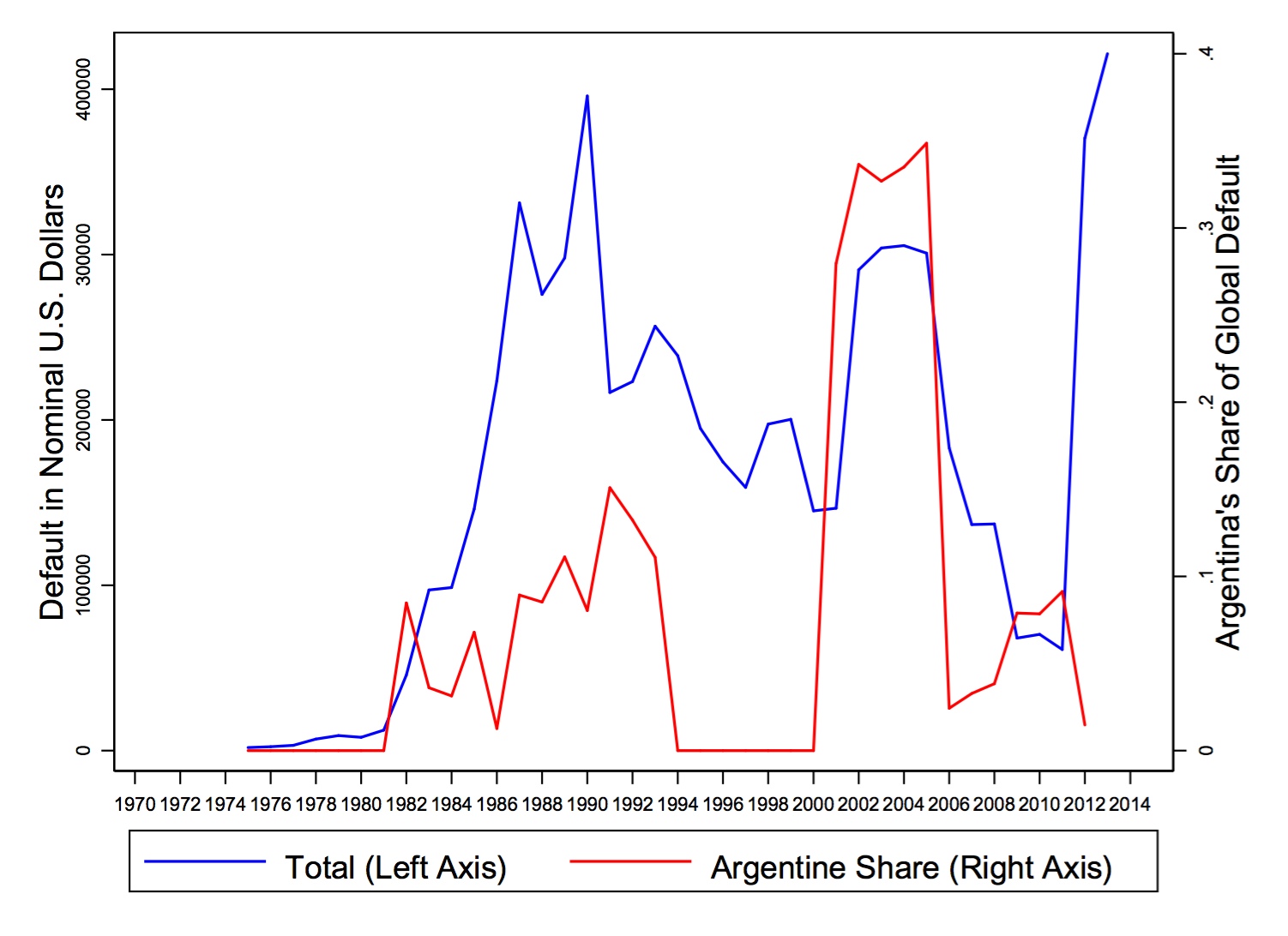

What’s interesting to me is the share of Argentine debt in default as a ratio of the total amount of debt in default globally. We can look at this too:

Perhaps one reason why Wednesday’s default is not such big news is that globally, Argentina is not unique these days, as it clearly was in the early 2000s.

Oh, and for another perspective on Argentina’s default, we can always read Oscar Wilde:

"This Argentine scheme is a commonplace Stock Exchange swindle" Oscar Wilde. An Ideal Husband (1895)

— lucas llach (@lucasllach) July 31, 2014