Indonesia’s capital city, Jakarta, is one of the largest urban agglomerations in the world. It is famously trafficky, polluted, and vulnerable to floods and other natural disasters. And for decades, Indonesian presidents have dreamt of a new capital city—like Brasília, Canberra, or Astana—that is more secure, more centrally located within Indonesia, and more livable.

Former president Joko Widodo brought these dreams closer to reality by announcing the creation of Nusantara, a new planned capital city located in the eastern part of the Indonesian portion of Borneo. Nusantara is envisioned to be a modern, green city that serves as the seat of the Indonesian government. Developed at the site of a former eucalyptus plantation, Nusantara will avoid some of the environmental challenges that Jakarta faces, and it will also be a more strategically defensible and geographically central capital city for this sprawling archipelagic state.

Nusantara is broadly popular—just like the former president himself. But building a new capital city in a remote area is difficult, and it will be costly. Given these costs, is Nusantara actually politically feasible, especially in a difficult budgetary environment? My coauthor Aichiro Suryo Prabowo and I answer this question in a new paper (available here), entitled “From White Elephant to White Whale: The Economics and Politics of Nusantara.” The title tells you our answer. Here is the abstract.

Indonesia’s new planned capital city of Nusantara is the most significant public works project in modern Indonesian history. We study the economics and politics of Nusantara from the perspectives of public finance and political economy. Combining data from official planning documents with a large body of original public opinion data, we find that the only plausible source of revenue for a project the size of Nusantara is the state budget, and that Indonesians do not support using state funds for this purpose. We discuss tradeoffs between infrastructural investment and other forms of public spending, and between present-day investment and future debt and tax burdens, in the context of a large public investment project of uncertain long-term value.

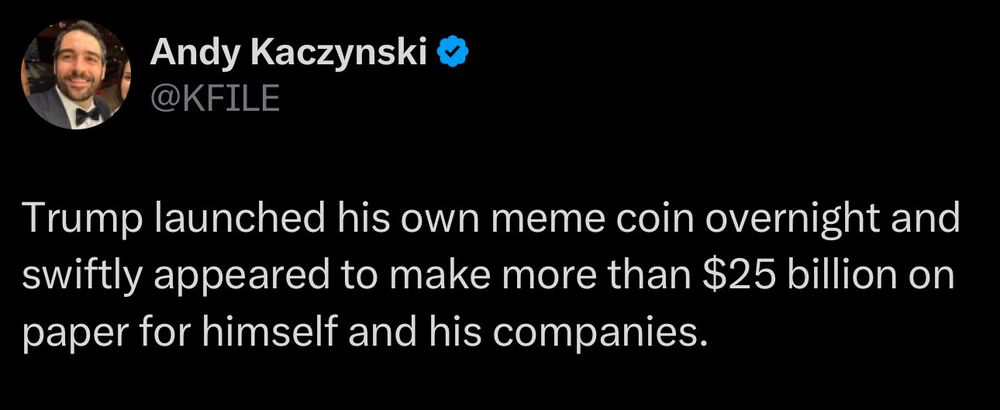

“US President-elect Donald Trump has launched his own cryptocurrency, which quickly soared in market capitalisation to several billion dollars.” This is the first sentence of a BBC story about $Trump, the new meme coin floated by a company “which has previously sold Trump-branded shoes and fragrances.” Coverage of this development has been interesting. The NY Times writes, “Trump Begins Selling New Crypto Token, Raising Ethical Concerns.” The Financial Times, by contrast, is brave enough to state it plainly: “The president-elect of the US is promoting a shitcoin?”

The word shitcoin is exactly the correct word for $Trump. But Trump’s shitcoin raises bigger questions about the future of crypto in the incoming administration, which faces no constraints whatsoever from the other branches of government when it comes to ethics, bribery, or even pretending to manage the conflicts of interest of all members of the executive branch.

What are these shitcoins about? Google shitcoin (turn off AI) if you want to learn the basics. I can summarize.

Do shitcoins have value? No.

Are shitcoins a grift? Yes.

Are they volatile, like, Ponzi-level volatile? Yes.

Are extremely wealthy people planning to use shitcoins to transfer wealth to themselves? Yes.

But shitcoins like $Trump have a political economy that is deeper than all that.

It is tempting to see shitcoins as a modern form of financial snake oil. But when the incoming president is promoting a shitcoin, it is not snake oil. $Trump is the Springfield Monorail. The difference is that snake oil salesmen exploit individuals, whereas shitcoins exploit communities. Snake oil buyers suffer individual consequences, whereas shitcoins have externalities with aggregate social consequences.

My conjecture is that most shitcoin-pushers are interested in a quick buck. But some have a much grander and more insidious ambition, and that is to become too big to fail.

Here is what I mean. Financial products have value to an individual because of their social value. A dollar is worth a dollar because it comes with the backing of a large and powerful state. A stock price reflects (OK, OK) the aggregate information about the value of the underlying asset. A shitcoin has value so long as people buying it think it has value—more precisely, it has value in the sense that people buying a shitcoin give it value. A rug pull is what happens when shitcoin-pushers exploit these dynamics.

An argument for free and unregulated markets in financial products is that competition weeds out bad investments and incentivizes people to make good investments. That is a good theoretical argument, but it is unrealistic as a description of actually-existing capital markets, which is why every developed capital market in the world is regulated in some fashion. Those regulations enable financial capitalism to work better. Deposit insurance, for example, encourages people to save rather than hide their money under their mattresses.

Implementing deposit insurance is a political action, a regulatory choice. Deposit insurance is a good idea because having people use banks rather than mattresses is a good idea, not just for them, but for the entire financial system. We know this because when the United States didn’t have deposit insurance, bank failures created bank runs which were bad for the entire financial system. You can repeat this story for any country in the world, for any type of saver or investor, in any type of financial product. The state intervenes to stabilize the financial system, because financial system health is a public good.

Most shitcoin-pushers are interested in quick rug pulls for quick bucks, and suckers be damned. Most ordinary investors and savers don’t care: a fool and his money are soon parted, and it’s great to know that you are 100% insulated from shitcoins if you are not a fool. But what would happen if a shitcoin-pusher were to attract investments from a substantial proportion of savers or institutional investors?

In that scenario, the collapse of a shitcoin would have systemic consequences. It would become necessary to bail it out.

I don’t mean that a collapse and bailout is going to happen right now. Those are just paper profits, and perhaps it’s just one big Saudi oligarch buying access. I mean, a shitcoin collapse is now on the table as possible future outcome in a world in which so much money is going into a shitcoin launched by the incoming president’s branded-fragrance-marketing subsidiary.

If you think that this is outlandish, remember the 2009 financial crisis and ensuing bailout. MBSes and CDOs and all those exotic financial products that rested on a house of cards? We all paid for the excesses of a few extremely powerful financial institutions. Even thought the greed and graft was plainly infuriating, there was no option but to bail them out. I supported the financial sector bailout then, and I still do today.

That is the greatest scam that you could ever imagine: exploiting as many individual savers and investors as possible, and then the federal government cleans up the mess. I think the biggest shitcoin-pushers know exactly what they are doing.

Barney Gumble: What about us brain-dead slobs? Lyle Lanley: You’ll be given cushy jobs.